Article

7 min read

How US Companies Handle Payroll When Remote Employees Work in a Different State

US payroll

Author

Shannon Ongaro

Last Update

June 09, 2026

Table of Contents

What is tax nexus, and why does it matter for remote teams?

How out-of-state employees affect your payroll obligations

Step 1: Classify your remote workers correctly

Step 2: Determine where your employees are actually working

Step 3: Register with the right state tax agencies

Step 4: Collect the correct tax forms

Step 5: Set up multi-state payroll withholding

Step 6: Choose a payment method that works for distributed teams

Step 7: Maintain payroll records and stay current with changing rules

What about international remote employees?

How Deel Payroll helps US companies with distributed teams

Key takeaways

- Any remote employee working from a state where your company has no office can create tax nexus there, triggering registration, withholding, and filing obligations in that state.

- Multi-state payroll compliance requires tracking each employee's physical work location, applying the correct state and local withholding rules, and registering with the right tax agencies before the first paycheck.

- Deel Payroll automates multi-state payroll tax calculations across all 50 states, so growing companies with distributed teams stay compliant without building an in-house tax department.

Your company is headquartered in Austin. Your best engineer works from Portland. Your newest sales hire just relocated to New Jersey — without telling HR first.

That's the reality for most US companies today. As of December 2025, 22.5% of US employees worked remotely at least part of the time. When those workers are spread across state lines, every single one of them creates new payroll obligations in the state where they sit and perform their work.

When a remote employee performs duties from their home state, they can create taxable presence — or "nexus" — for their employer in that state, even if the company has no office, property, or other operations there.

This results in payroll registration requirements, state income tax withholding obligations, state unemployment insurance accounts, and in some cases, workers' compensation obligations in every state where you have a remote worker.

If your team is distributed across multiple states, this guide walks you through exactly how to handle it.

What is tax nexus, and why does it matter for remote teams?

Tax nexus is the legal connection between a business and a state that gives that state the right to tax the company and impose compliance obligations. For most of business history, nexus was created by physical presence, such as a store, an office, a warehouse.

Remote work changed that.

A 2012 New Jersey Superior Court ruling — Telebright Corp. v. Director, New Jersey Division of Taxation — established that a single remote worker performing services from their home in a state was sufficient to subject an out-of-state employer to that state's corporate tax. That principle has since been widely upheld.

For employers, nexus creates a cascade of obligations: registering as an employer in that state, setting up payroll tax accounts, withholding state income tax from each paycheck, filing quarterly payroll returns, and paying state unemployment insurance contributions.

Getting this wrong is costly. Under-withholding, late registrations, and missed filings all carry penalties and interest in every state where you're non-compliant.

How out-of-state employees affect your payroll obligations

When you hire — or retain — an employee who works from a state where you have no existing presence, here's what typically follows:

Payroll tax registration: You'll need to register as an employer with that state's revenue department and department of labor. Most states require registration before or at the time of the first paycheck.

State income tax withholding: Payroll withholding generally follows where the employee physically performs their work. That means calculating and withholding state income tax based on the employee's home state rules — not your company's home state rules.

State unemployment insurance (SUI/SUTA): You'll owe unemployment insurance contributions in the state where the employee works. Rates vary significantly by state and by your company's claims history in each jurisdiction.

Workers' compensation coverage: Most states require workers' compensation insurance for employees working within their borders, regardless of where the employer is based.

Potential "convenience of the employer" rules: A growing number of states apply what's known as a "convenience of the employer" rule that may tax wages as if the employee worked at the employer's office state, not the employee's home state, unless the remote arrangement exists for the employer's business necessity.

Step 1: Classify your remote workers correctly

Before you set up payroll for any remote worker, confirm their classification. The two categories that matter most are employee vs. independent contractor and in-state vs. out-of-state.

Employee or independent contractor?

This is the foundational question. Misclassifying an employee as an independent contractor can result in severe penalties, back taxes, and personal liability for company leadership.

Employees receive payroll tax withholding, employer-paid payroll taxes (FICA, FUTA, SUTA), and state-mandated benefits. Independent contractors handle their own taxes and receive a 1099-NEC at year end instead of a W-2.

Some companies opt to engage remote workers in other states as independent contractors specifically to sidestep multi-state payroll registration. That's a risky strategy; if the working relationship looks like employment, states will treat it that way, regardless of what the contract says.

In-state or out-of-state?

If the employee lives and works in the same state as your registered business location, your standard state payroll setup applies. If they live and work in a different state — even one where you have no office — you have new obligations in that state.

Global Hiring Toolkit

Step 2: Determine where your employees are actually working

This is where many companies fall short. Employees move. They work from vacation homes. They split time between cities. Each of those scenarios can create new obligations.

To stay compliant, you need to know — in real time — where each remote employee is physically performing their work. That means:

- Requiring employees to report address and work location changes before they take effect, not after

- Tracking days worked by state for any employee who splits time between states (this matters for income tax apportionment)

- Updating your payroll system to reflect current work locations, not hire-date locations

Maintain detailed records of employee locations, hours worked, and any changes in residency status, particularly when workers split time between states.

Deel's HRIS

Step 3: Register with the right state tax agencies

Once you've confirmed you have a remote employee in a new state, register as an employer in that state before processing their first paycheck. In most states, this involves:

- Registering your business with the state's department of revenue (for income tax withholding)

- Registering with the state's department of labor or workforce commission (for unemployment insurance)

- Obtaining workers' compensation coverage that covers that state

- Registering with any applicable local tax jurisdictions (some cities and counties have their own payroll taxes)

Timelines vary. Some states process registrations quickly; others take weeks. Build registration lead time into your hiring process when you know a new hire will be in an unfamiliar state.

Step 4: Collect the correct tax forms

The federal forms you need depend on whether the worker is an employee or contractor, and whether they're US-based or international.

US employees

- At hire: IRS Form W-4: Your new employee fills this out to authorize federal income tax withholding. Many states also require a separate state withholding form

- At year end: Form W-2: Reports wages paid and taxes withheld for the calendar year

US independent contractors

- At hire: IRS Form W-9: Collects the contractor's taxpayer information

- At year end: Form 1099-NEC: Reports the total amount paid to the contractor during the year (required if you paid $600 or more)

International independent contractors

- At hire: IRS Form W-8BEN: Confirms the contractor's foreign status and identifies any applicable tax treaty

- **At year end: Foreign contractors who provide a valid W-8BEN are generally exempt from US 1099-NEC reporting requirements. Keep the W-8BEN on file. If any portion of the contractor's services were performed inside the US, consult a tax advisor about whether reporting obligations apply.

For international employees, the process is more complex. You won't use US tax forms for workers employed through a local entity or employer of record. Their withholding and filings are governed by the laws of the country where they work.

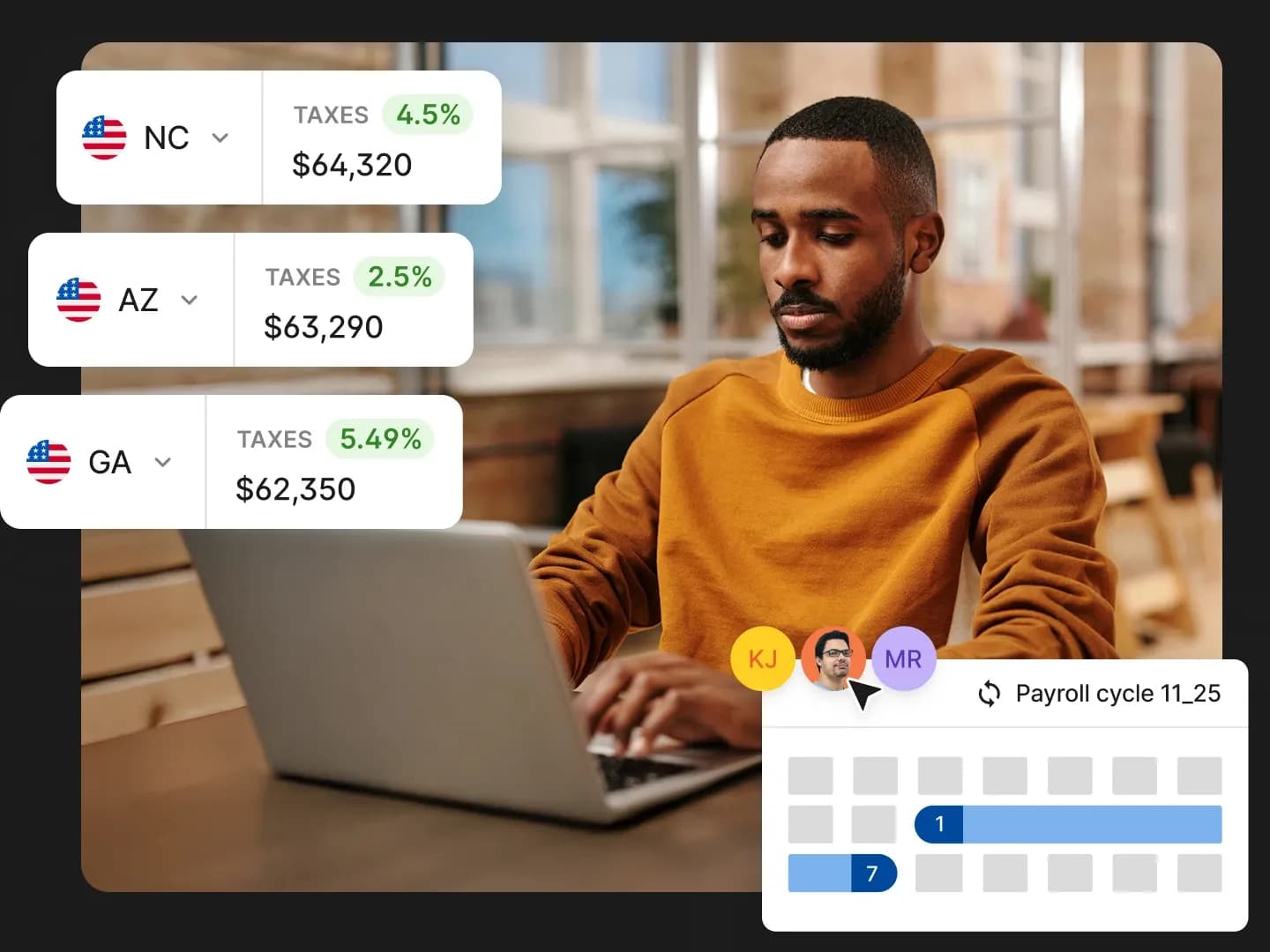

Step 5: Set up multi-state payroll withholding

Multi-state payroll withholding means calculating the correct state and local income tax withholding for each employee based on where they actually work, not where your office is.

State income tax rules vary significantly. Some states have no individual income tax on wages — including Florida, Texas, Nevada, Washington, Wyoming, South Dakota, Alaska, Tennessee, and New Hampshire. Others have complex graduated rate structures. Some cities and counties layer additional local income taxes on top of state taxes.

Key things to get right:

Reciprocal agreements

Some neighboring states have reciprocal tax agreements that allow workers to pay income tax only in their home state, even if they work across state lines. If your employee's home state and work state have a reciprocal agreement, withholding stays in the home state. Without one, you may need to withhold for both.

Multi-state employees

For employees who work in multiple states during the year, wages generally need to be allocated to each state based on the time spent working there. Your payroll system must track and split this correctly.

Convenience rules

As mentioned above, states like New York apply their own rules that can supersede the standard "where the work is performed" standard. Always check the specific rules for each state where you have employees.

Deel Payroll - US

Step 6: Choose a payment method that works for distributed teams

Most US-based employers use direct deposit as the primary payment method. It's reliable, widely accepted, and meets most state requirements for timely payment. State laws govern how frequently you must pay employees, so confirm the pay frequency rules in each state where workers are located.

For international team members, additional options include SWIFT bank transfers, digital wallets, and cryptocurrency payouts (where legally permitted). Payment method availability varies by country, and some countries require wage payments in local currency.

Step 7: Maintain payroll records and stay current with changing rules

The IRS requires keeping employment tax records for at least four years after the due date of the tax or the date you paid it, whichever is later; the Small Business Administration recommends six. State requirements may differ, as some states have longer retention requirements.

Beyond record-keeping, multi-state payroll compliance requires staying current. State tax rates, thresholds, reciprocal agreements, and withholding requirements change regularly. What applied last year may not apply today. This is the compliance burden that grows with every new state you enter, and it's compounding for most distributed companies.

Deel has in-house payroll and compliance experts who monitor regulatory changes across jurisdictions and notify customers in advance of upcoming updates.

What about international remote employees?

When an employee works from a different country, you can't simply add them to your US payroll, as you'd be applying US withholding rules to someone who doesn't live or work in the US.

You have three main options:

Hire them as independent contractors

Simpler administratively, but only appropriate if the working relationship genuinely qualifies. Misclassification risk still applies, and different countries define the employee/contractor distinction differently.

Establish a local entity

Opening a foreign subsidiary in the worker's country lets you hire them as a local employee. This is the most compliant approach but requires time, legal resources, and ongoing local administration.

Use an employer of record (EOR)

An EOR is a third party that legally employs your international workers in their home country, handling local payroll, tax withholding, statutory benefits, and compliance. You retain control of the day-to-day work; the EOR handles the legal employment relationship and all the associated obligations.

See how you can easily hire employees globally with Deel.

How Deel Payroll helps US companies with distributed teams

Managing payroll for a remote, multi-state US team is fundamentally a compliance problem. Every new state adds registration requirements, withholding calculations, filing obligations, and monitoring responsibilities. For most growing companies, building the in-house expertise to manage this across all 50 states isn't practical.

That's what Deel Payroll is built for.

While we were very comfortable with hiring locally, we were apprehensive about the costs and legal responsibilities for compliance in the United States. We didn’t want to hire full-time HR people to figure out things like health benefits and filing tax returns with the IRS. Now we know we can trust Deel to manage the complexities.

—Matthew Buchanan,

CEO, Letterboxd

Deel Payroll for the US handles payroll across all 50 states from a single platform. It automatically calculates multi-state payroll taxes and syncs direct deposits and payslips with accounting software — so your team gets paid accurately and on time, in every state where they work.

Here's what that means in practice:

- Automatic multi-state tax calculations: Deel Payroll instantly calculates the correct federal, state, and local payroll taxes for each employee based on their registered work location — across all 50 states, including those with complex local tax structures

- Continuous compliance: Tax rules change. Deel applies regulatory updates automatically — so you're not manually tracking rate changes across dozens of jurisdictions. This is what Deel calls continuous compliance: tax rules and regulatory changes applied automatically, not retroactively

- Benefits administration, connected: PEO manages benefits enrollment and administration — including medical, dental, vision, and 401(k) — alongside payroll for co-employed workers. For Deel Payroll US clients, benefits administration is available through connected integrations including Employee Navigator

- Owned infrastructure, not aggregated: Unlike providers that aggregate third-party processors, Deel processes payroll on its own infrastructure — which means faster issue resolution, clear accountability, and no broken handoffs between vendors

- HR and compliance support: If your US team is growing but not yet ready to manage multi-state employer registrations independently, Deel lets you co-employ your US workers through PEO. Deel handles state registrations, employer tax contributions, and benefits as the co-employer while you retain full control of day-to-day management

Deel processes $22 billion in payroll annually and serves 40,000+ customers in 150+ countries. For US companies managing distributed domestic teams — or a mix of US and international workers — Deel provides a single system of record that handles payroll, compliance, HR, and benefits without a patchwork of vendors.

Want to see how it works for your team? Book a 30-minute demo of the platform with an expert.

Deel Payroll - US

Stay compliant, save time, and pay your US team with confidence

Deel on G2

FAQs

How do US companies handle payroll when employees work in a state where the company has no office?

When a remote employee works from a state where the employer has no established presence, the employer typically needs to register as an employer in that state, set up payroll tax withholding accounts, withhold the correct state and local income taxes from each paycheck, and pay state unemployment insurance contributions. This applies regardless of whether the company has an office, employees, or any other operations in that state. The employee's physical work location is sufficient to create these obligations.

Does having one remote employee in another state create tax nexus?

In almost all cases, yes. A single remote employee performing services from their home state creates taxable nexus for the employer in that state. This was established as far back as 2012 in New Jersey courts and has since been widely affirmed. Nexus created by a remote worker triggers registration, withholding, unemployment, and potentially workers' compensation obligations in the employee's work state.

What are convenience of the employer rules and which states apply them?

The "convenience of the employer" rule is applied by a number of states to determine which state's income tax applies to a remote worker's wages. States with full convenience rules include New York, Delaware, Pennsylvania, and Alabama. New Jersey and Connecticut apply reciprocal versions, meaning the rule only applies to residents of states that impose similar rules. Oregon applies a limited version for nonresident managerial employees only.

Under these rules, if an employee works remotely for their own convenience (not because the employer requires it for business reasons), their wages may be taxed as if they worked at the employer's office location, even though the employee is physically in another state.

This is particularly significant for companies headquartered in New York, which aggressively applies this doctrine. Note that Nebraska's rule was modified in 2024 and now only applies if the nonresident employee is physically present in Nebraska for more than seven days during the tax year.

How do payroll tax withholding rules differ for employees in multiple states?

For employees who split their working time between two or more states, wages are generally allocated and withheld based on the proportion of time spent working in each state. Some state pairs have reciprocal agreements that simplify this by allowing withholding only in the employee's home state.

Employers need to track days worked by state and configure payroll systems to split withholding accordingly. This is one of the more complex payroll scenarios for multi-state US companies.

What is the difference between Deel's payroll solutions for US employers?

Deel Payroll - US is a full-service payroll platform that allows companies to run payroll across all 50 states, with automatic tax calculations and multi-state compliance. Benefits administration is available through connected integrations such as Employee Navigator. It's suited for companies that want to manage their own payroll with automated compliance support.

PEO is a co-employment model: Deel becomes the co-employer for your US workers, handling state registrations, employer tax contributions, and benefits — including medical, dental, vision, and 401(k) — while you maintain control of day-to-day management. PEO is often a fit for smaller or faster-growing teams that don't yet want to manage multi-state employer registrations themselves.

How should companies handle payroll for international remote employees?

US payroll rules don't apply to employees who live and work in another country. International employees require payroll set up under the laws of their country of work, including local tax withholding, statutory benefits, and employment compliance.

Companies have three main options: engage international workers as independent contractors (with misclassification risk), establish a foreign entity in the worker's country, or use an employer of record (EOR).

An EOR handles local employment, payroll, and compliance on the company's behalf. Deel's EOR service covers 150+ countries on owned infrastructure, with no third-party processors.

Disclaimer: This information is provided for informational purposes only and should not be considered tax or legal advice. Consult a qualified tax professional for guidance specific to your situation.

Shannon Ongaro is a content marketing manager and trained journalist with over a decade of experience producing content that supports franchisees, small businesses, and global enterprises. Over the years, she’s covered topics such as payroll, HR tech, workplace culture, and more. At Deel, Shannon specializes in thought leadership and global payroll content.